For those of us who have spent decades in this industry, the year 1999 is a memory that defines us. It was a moment of global panic, a digital apocalypse known as the Y2K bug. While the world braced for chaos, we in India saw an unprecedented opportunity. Over a few short months, a nation of engineers — many with little more than a landline and a fervent work ethic — stepped up.

We wrote billions of lines of code, patched legacy systems, and proved that a large-scale, offshore delivery model could work. That moment wasn’t just a project; it was our baptism that laid the foundation for the next thirty years of growth, opening doors that were once firmly shut.

The journey that followed was a saga of grit. We fought to overcome customer frustrations and skepticism. The early days were a battle of wits, managing unreliable infrastructure and proving that a remote team could be as good, if not better, than an on-site one. We evolved from mere “body shoppers” to strategic partners, moving from a rigid Software Development Life Cycle (SDLC) to nimble, agile models.

Then came the 2008 global financial meltdown. When banks and businesses in the US and Europe were on the verge of collapse, it was the Indian IT sector that stepped up. Our value proposition was no longer just about cost; it was about resilience. By providing critical, round-the-clock support and helping businesses cut costs, we became an indispensable pillar of the global economy. For many of us, this was a moment of vindication — the world had come to rely on us. We even went so far as to rewrite payment agreements to provide indirect financing, supporting our customers when they needed it most.

Today, however, the script has changed.

Reading the Market: What the IT Index Tells Us

For years, the Nifty IT Index has been a bellwether of India’s tech strength. But 2025 has been a reminder that markets move faster than boardrooms. The index is down significantly year-to-date, a stark contrast to the modest decline of the broader Nifty50. This performance gap is a real-time scoreboard of strategic direction.

The pressure is real. Foreign investors have pulled out more than ₹50,000 crore from Indian IT stocks this year. If we are to believe, we need to understand that the capital pursues the creators of AI, not just the implementers. This makes many in Mumbai’s trading circles whisper that the golden age of cost arbitrage is ending.

This market behavior is a valuation reality check. Manish Chokhani, Director of Enam Holdings, points out that top U.S. tech companies earn such massive profits that they can trade at a premium — pulling capital away from markets like India. When investors can choose between architects and builders of new tech, capital gravitates toward the perceived creators of greatest value.

Some are punished more harshly, others less so — but the market is drawing a line. For much of the last decade, the Nifty IT Index enjoyed a premium over the Nifty50. In 2025, that premium hasn’t just narrowed — it has flipped. Investor faith in Indian IT is no longer about scale; it’s about clarity of future direction.

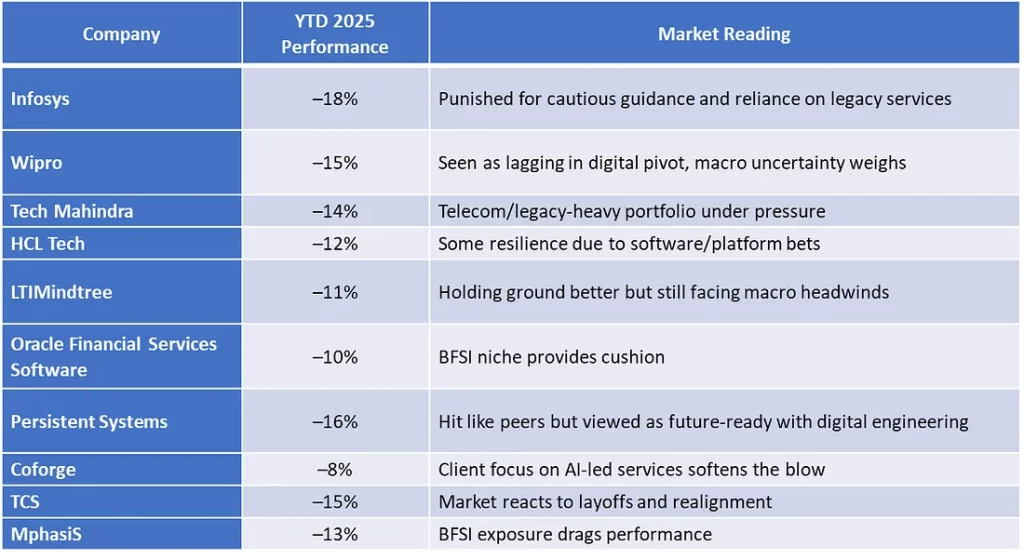

Look closer at the constituents, and the divergence is striking:

Underperformers: Infosys (–18%) and Wipro (–15%) have seen sharp declines despite reporting solid Q1 2025 results. Analysts flagged Infosys’s downgraded FY26 revenue guidance (0–3% constant currency) as cautious, damping sentiment. Wipro too has guided for slower-than-peer growth, reinforcing investor concerns. As Reuters noted, muted guidance from legacy giants underscores their vulnerability in a tighter spending environment.

HCLTech (–12%): The stock fell nearly 10% in a single day in January after missing Q3 revenue estimates and raising only the lower end of its annual outlook. According to Reuters, eleven brokerages downgraded the stock and cut price targets, citing continued weakness in software demand.

Tech Mahindra (–14%): Its Q1 results showed a 34% YoY PAT surge and margin expansion, but the profit missed Street expectations, triggering a 2% stock dip. Economic Times and Reuters both linked this to tempered performance in the Americas and muted revenue growth, illustrating that even strong operating metrics can’t offset investor doubts about long-term trajectory.

Differentiated Declines: Persistent Systems (–16%) and Coforge (–8%) are also in negative territory, but the interpretation is different. As Reuters reported, mid-tier firms are gaining market share from industry goliaths by offering cost-effective, outcome-driven deals, especially in a discretionary spending environment. Economic Times added that investors view these firms as agile, niche-focused players better positioned to capture AI-led growth. Their declines reflect sector-wide headwinds, but the narrative surrounding them is more forgiving.

For CXOs, this divergence is not background noise; it’s a scoreboard. Scale no longer guarantees reward — clarity of direction does. If clients and investors are signaling that specialization and AI integration drive value, leadership cannot afford to treat today’s slump as just another cyclical downturn.

The Bullish Counterpoint: A Transition, Not a Decline

There is, however, another way to read the data. EY’s 2025 survey suggests GenAI could lift productivity in India’s IT sector by as much as 45% over the next five years, with software development roles seeing nearly 60% gains. This isn’t just margin improvement; it’s the promise of a new operating model.

The industry’s leaders echo this optimism. Infosys CEO Salil Parekh is a strong proponent of the view that AI will not lead to net job losses. As he told PTI, “At this stage, my sense is that the technology will help business to grow even further as opposed to anything else. We don’t see any layoffs in Infosys with these new-age technologies.” This echoes the company’s strategy of aggressively reskilling its employees to meet the evolving demands of clients.

NASSCOM adds further evidence. By July 2025, it reported that 1.5 million Indian IT professionals had already been trained in AI and GenAI skills, with nearly 100,000 holding advanced certifications. That’s not defensive reskilling — it’s proactive repositioning at scale.

Goldman Sachs, however, adds a dose of realism. It projects India could create 2.3 million AI-linked jobs by 2027, but warns that only half of that demand will be met with job-ready talent. This paradox — abundance of people but scarcity of skills — is both our Achilles’ heel and our chance to lead.

And clients are ready. Microsoft’s 2025 Work Trend Index for India shows that a remarkable 93% of Indian business leaders plan to use AI agents within 18 months. This indicates that AI is no longer an experiment for Indian firms but is becoming a scaled operational tool. As TCS CEO K. Krithivasan noted, the company is seeing a significant uptick in demand for “AI for business,” where clients are looking to deploy AI across their value chains to improve customer experience and speed.

The Unspoken Threat: The Education–Employability Paradox

While the industry pivots, a fundamental challenge remains: India’s engineering education system. It has long operated as a factory model, churning out approximately 1.5 million engineering graduates each year. On paper, the syllabus of a top-tier IIT might look identical to that of a suburban engineering college, but the outcomes are miles apart. The system prioritizes rote learning and exam-passing over the critical thinking and problem-solving skills the industry desperately needs.

The result is a profound skills gap. A recent Mercer-Mettl analysis revealed that a mere 42.6% of Indian graduates are considered “employable.” This is not an indictment of the talent pool but of a system that fails to prepare them for the realities of the modern workplace. The paradox is clear: even as AI is set to create 2.3 million new jobs in India by 2027, according to Goldman Sachs, only half of that demand will be met with job-ready talent.

To overcome this, the education system must shift from rote memorization to inquiry-driven, critical thinking; modernize curricula to embed AI, data science, and cybersecurity as core subjects rather than electives; and mandate industry-led projects and internships to bridge academia with real-world practice.

Strategy for the C-Suite: From Manpower to Intelligence

So, where does this leave the CEOs and boards steering India’s IT giants? The path forward requires a pragmatic, two-pronged approach.

1. The Hype Cycle: A Strategic Opportunity

As per Gartner’s 2025 AI Hype Cycle, Generative AI is now moving from the “Peak of Inflated Expectations” to the “Trough of Disillusionment.” This is a pivotal moment. The initial buzz is fading, and clients are now faced with the hard realities of implementation — data security, governance, and integrating AI into complex legacy systems. This is where our expertise shines. We are the masters of enterprise-scale systems. We don’t just offer a tool; we offer a secure, scalable, and practical roadmap to transform a concept into a core business asset.

2. The Global Ecosystem: Our Indispensable Role

For hyperscalers like AWS, Google, and Microsoft, India’s IT firms are not mere subcontractors; they are the go-to-market engine that opens new geographies and the implementation backbone that turns a license into a living system. They sell the license; we do the heavy lifting of making their products work in messy, complex, real-world enterprise environments. This mutually beneficial model, pioneered by Indian IT, has created a global ecosystem where the OEM, the Indian partner, and the customer all thrive. As Infosys CEO Salil Parekh stated, the company has “powerful partnerships with the hyperscalers,” and their growth is “aligned to the hyperscalers’ growth.”

3. The Indian Talent Moat vs. U.S. Policy Headwinds

While policy headwinds like the proposed U.S. HIRE Act threaten to impose a 25% tax on outsourcing, the reality is that America cannot replicate India’s talent depth overnight. The HIRE Act is a political gesture, not an economic solution. As Phil Fersht of HfS Research notes, the sheer scale of India’s AI-ready talent — over 13 million skilled workers by some estimates — is not just an advantage; it is an irreplaceable moat that global firms will continue to rely on. Any attempt to build that capacity domestically would inflate costs and slow innovation.

4. From Services to Platforms: Beyond Selling Hours

The most significant strategic pivot is from a services-only model to one that includes high-margin platforms and products. HCLTech’s bet on IBM’s software assets is a prime example. But they are not alone. Infosys has long been a pioneer with Finacle, a banking product suite that serves over a billion people and millions of businesses in more than 100 countries. Similarly, TCS has its BaNCS platform for the banking and financial services industry, used by over 450 institutions worldwide. Wipro has also entered the fray with its HOLMES AI platform, an engine for intelligent automation. These are not mere services; they are strategic assets that generate recurring, high-margin revenue. The imperative for this shift is clear from the top. HCL Tech CEO C. Vijayakumar put it bluntly to The Economic Times, urging the industry to be “proactive” because “if you do not do it somebody else will do it.”

The Pragmatic Outlook

The Indian IT industry is not facing an obituary; it is undergoing a profound metamorphosis. Goldman Sachs estimates India could generate 2.3 million AI-linked jobs by 2027, though only about half that number will be filled with ready talent. That gap is both a risk and an unprecedented opportunity. Meanwhile, India’s AI market is projected to grow fifty-fold by 2030. The long-term direction of travel is unmistakable.

In 1999 and again in 2008, Indian IT proved it could rise when the world faltered. 2025 is another such moment. The question is not whether Indian IT will survive — it will. The question is whether your board will pivot boldly enough to define what that survival means. The winners will be those that convince clients — and the markets — that their value lies not in cheaper delivery, but in smarter, AI-powered problem-solving. The world no longer needs India to code. It needs India to co-create.

###

Disclaimer

The information and opinions expressed in this blog post are for general informational and educational purposes only. They are based on publicly available data, news reports, and industry analysis as of September 2025. This content does not constitute financial, tax, or legal advice. Readers should not rely solely on the information provided here for making any business, investment, or personal financial decisions. Always consult with a qualified professional for advice tailored to your specific circumstances. The author and publisher are not liable for any losses or damages arising from reliance on the information contained in this article.

References:

- Nifty IT Index vs. Nifty50 Performance: This data is from financial market data providers.

- Financial Market Data: National Stock Exchange of India (NSE), Reuters, The Economic Times.

- Research & Analysis: EY, Gartner, NASSCOM, Goldman Sachs, Mercer-Mettl, HfS Research, Enam Holdings.

- Leadership Commentary: K. Krithivasan (TCS), Salil Parekh (Infosys), C. Vijayakumar (HCLTech)— The Economic Times, Reuters, Press Trust of India (PTI).

Leave a Reply